The Rise And Rise Of Land Tax In Australia

Owners of residential land in Australia may face unexpected land tax bills in the coming 12 months given recent land tax changes particularly in New South Wales and Queensland. This article summarises the key changes (as at September 2022) that land owners and potential property investors need to be aware of.

New South Wales – surcharge land tax to double

Under land tax rules in New South Wales, certain land owners may face a hefty land tax bill when the foreign owner surcharge land tax increases from 2% to 4% next year (i.e. on land owned at midnight on 31 December 2022). The tax applies to land owners that are deemed “foreign persons”.

Are you deemed a “Foreign Person”?

A land tax surcharge, referred to as the “foreign owner surcharge land tax” (FOSLT) applies to certain land owners that are classified as “foreign persons” and hold residential land in New South Wales.

A land owner is by default considered a “foreign person” unless the land owner:

- Is an Australian citizen; or

- Has lived in Australia for 200 days or more in the 12 months prior to the taxing date of 31 December, and the land owner is:

- a permanent resident of Australia; or

- a New Zealand citizen that holds a subclass 444 visa

Unlike the general land tax charge, there is no tax free threshold under the FOSLT.

What does this mean in practice?

In short, the FOSLT means that absences from Australia can result in a hefty foreign surcharge land tax bill on top of ordinary land tax.

For foreign residents living offshore and classified as “foreign persons” under the FOSLT, their land tax bill for residential land they own in New South Wales will effectively double to 4% for the next land tax year.

Similarly, for permanent residents (including certain New Zealanders) living in Australia but for whatever reason will be out of Australia for more than 5 months during a calendar year there may also be a hefty foreign surcharge land tax bill imposed during their period of absence.

The FOSLT can also be levied even if the land relates to a permanent resident’s main residence. That said, a main resident exemption can be applied for if the permanent resident uses or intends to occupy their main residence for a continuous 200 day period during the land tax year. This exemption can be applied online by 31 March in the relevant tax year.

Queensland – Interstate holdings now need to be declared

Starting from 1 July 2023, the Queensland Government will calculate land tax using a formula that include land values in interstate land. This is a significant change in calculating Queensland land tax and now differs considerably in approach when compared to other states and territories.

For land owners that have Australian land holdings outside Queensland, this potentially means their Queensland land holdings will now be subject to higher Queensland land tax from 1 July 2023.

In particular, when calculating Queensland land tax payable, the total value of Australian land (subject to certain exclusions) will be used to determine:

- whether the tax-free threshold has been exceeded (currently the threshold for individuals is $600,000 {other than absentees} and $350,000 for other holding entities including absentees); and

- that rate of land tax that would be applied to the Queensland portion of land holdings

What interstate land can be excluded?

The new rules state that certain interstate land can be excluded which include.

- Main residence

- Primary production

- Supported accommodation

- Moveable dwelling (caravan) park

- Retirement village

- Transitional home

- Charitable institutions

- Aged care

The Queensland government has indicated that further information on the exclusions will be available after 30 June 2023.

How do the new rules work?

This is best illustrated by way of example.

Assume a resident individual property investor owns the following land holdings as at 30 June 2022 and as at 30 June 2023:

- Investment property in Brisbane, Queensland with a taxable land value of $590,000

- Investment property in Sydney, New South Wales (NSW) with a taxable land value of $2,000,000

For the 30 June 2023 land tax year, no land tax in Queensland would be payable as only the value of Queensland property is taken into account as at 30 June 2022. This is because the value of the Queensland property is under the current land tax threshold of $600,000.

For the 30 June 2024 land tax year, the Queensland land tax would be calculated as follows:

- Total taxable value of land in NSW and Queensland as at 30 June 2023: $2,590,000 ($590,000 + $2,000,000)

- Hypothetical land tax liability on $2,590,000: $30,735 (calculated based on rates tables)

- The Queensland land tax liability is then calculated as the proportionate taxable value of the Queensland land as a percentage over total taxable land multiplied by the hypothetical land tax liability being:

$590,000 / $2,590,000 x $30,735 = $7,001.

In the above example, an additional $7k in land tax is payable by the property investor because of the change in the land tax rules.

Making the declaration of interstate land

Under the new rules, interstate land owners that also own land in Queensland will now need to declare their interstate land holdings. This declaration will need to be completed from 30 June 2023 by the earlier of:

- within 30 days of receiving a land tax assessment notice

- on or before 30 October

In valuing interstate land, the new rules require the valuation to be determined by valuation legislation in that particular state or territory.

The declaration is to be made online by setting up a “QRO Online account”.

Other states and territories – watch out for the land tax surcharge

While there have been no recent and significant land tax changes in the other states and territories, it will be important for land owners who own land across Australia to be mindful of the land tax rules across the state and territories and in particular land tax surcharges.

A number of states and territories now have a land tax surcharge which can be triggered based on certain factors such as where the property owner is absent from Australia; classed as a foreign person or relating to certain trusts.

From next year, New South Wales will have the highest rate of land tax surcharge of 4% as noted above followed by Victoria, Queensland and Tasmania where the land tax surcharge rate is levied at 2% subject to meeting certain criteria in that particular state / territory.

Currently, Western Australia and Northern Territory do not have any land tax surcharge levied on land owners with the Northern Territory the only state/territory that does not have any land tax levy.

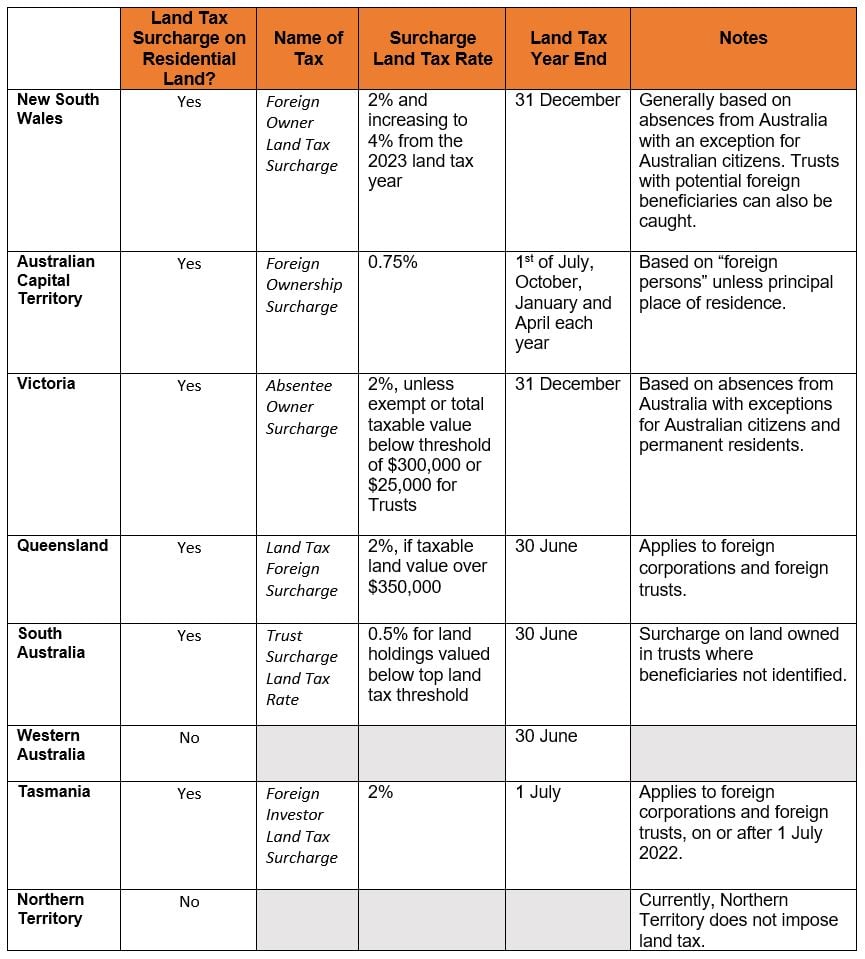

A quick summary of land tax surcharges

The table below provides a quick summary of the land tax surcharges on residential land in each state and territory where applicable, which is in addition to the land tax payable if a property in not a principal place of residence or otherwise exempted. For further details, see the links below.

Summary – land tax surcharge

References:

Australian Capital Territory: https://www.revenue.act.gov.au/land-tax/foreign-ownership-surcharge#:~:text=If%20you’re%20a%20foreign,your%20principal%20place%20of%20residence

Queensland: https://www.qld.gov.au/environment/land/tax/interstate

https://www.qld.gov.au/environment/land/tax/calculation/individuals

South Australia: https://www.revenuesa.sa.gov.au/landtax

Western Australia: https://www.wa.gov.au/organisation/department-of-finance/land-tax

Tasmania: https://www.sro.tas.gov.au/land-tax

Northern Territory: https://treasury.nt.gov.au/dtf/territory-revenue-office

Want to know more about how Bentleys can help you?

Make a time for a chat with us today. We’re here to help you get where you want to be.

Disclaimer: This information is general in nature and should not be relied on as advice. It does not take into account the objectives, financial situation or needs of any particular person. You need to consider your financial situation and needs and seek professional advice before making any decisions based on this information.

Send enquiry

We’d love to hear from you. Complete the form and someone from our team will contact you soon.