Sequencing Risk And The Impact On Your Investments During Retirement

Are you retired or about to retire? Are you unsure of the volatility of your assets?

For many people who are about to retire or have not had much experience with investing, assessing your investment choices can be a daunting process.

Often, the average return shown in performance tables of investment managers and superannuation funds can be misleading.

Often, these tables give the impression that returns are mostly linear or in a straight line that varies only on a quarterly or annual basis.

However, the reality with all investments is that there is a certain amount of volatility, be that large or small. Many people perceive growth assets such as shares to be more volatile, and defensive assets such as fixed interest and cash to be less volatile.

What is sequencing risk and why does It matter?

Sequencing risk is the risk of large losses occurring to an investment portfolio at a time when it is difficult to recoup them. For example, if you are retired (or about to retire) and experience a prolonged investment drawdown, such as the GFC (mid-2007 to early 2009); drawing an income to fund your retirement at this point will impact the longevity of your investment portfolio.

To fund your retirement, you would be selling investments (i.e., shares or managed fund units) in a market drawdown. This would then mean you have less investments (i.e., shares or managed fund units) remaining when investment markets recover.

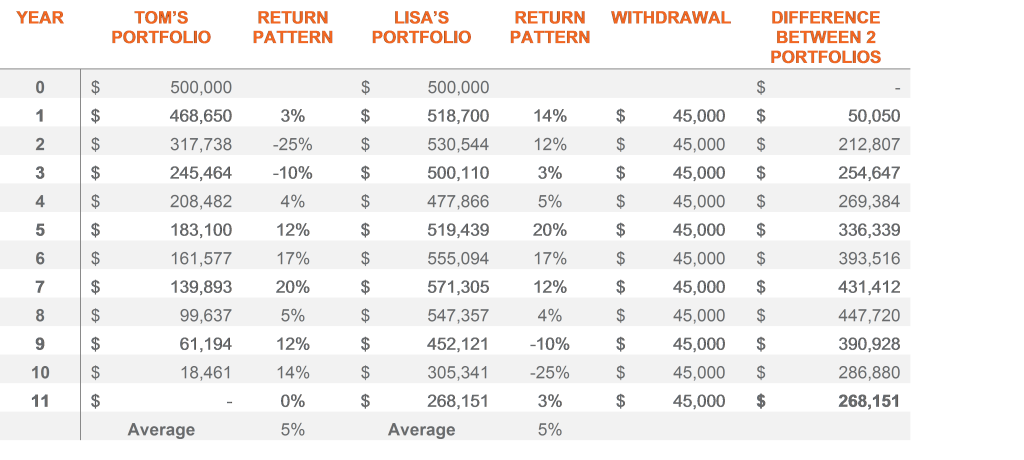

In the table below we outline a situation where sequencing risk impacts the portfolio of two parties in very different ways.

The below illustrates the scenario of someone retiring with a superannuation balance of $500,000 (both Tom and Lisa). In both cases, there is an average rate of return of 5% over 11 years, and annual drawings of $45,000.

However, in this example, Tom’s portfolio is impacted by larger drawdowns in the initial years. This shows very clearly how large drawdowns early into retirement can result in very different outcomes.

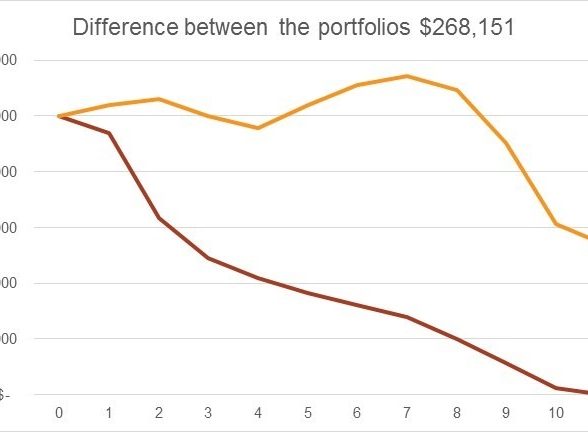

At the end of year 11, the difference between Tom’s and Lisa’s portfolio is $268,151, despite having the same average return of 5%. This demonstrates how the average rate of return can be a misleading way of assessing performance. Furthermore, Tom’s investment portfolio is exhausted in year 11, whereas Lisa’s investment portfolio is valued at $268,151 in year 11.

The impact of sequencing risk:

This example is for illustrative purposes only.

The impact of sequencing risk:

This example is for illustrative purposes only.

So, how can you reduce sequencing risk?

The timing of investment market drawdowns can dramatically impact the length of time a retiree’s capital will last (as per the example of Tom).

The good news is that there are ways to structure investments for retirees to manage this risk. These include:

- Diversification into uncorrelated asset classes and holding cash to reduce withdrawals from growth investments during heavy market drawdowns.

- Direct investment distributions to cash or conservative investment options. However, this may only be available with some types of retirement structures, such as SMSFs and Wraps. Pooled funds and industry funds may not offer this functionality.

Investors who are exposed to sequencing risk in early retirement may need to work longer or reduce their living costs, so having an effective plan to manage this risk is essential.

To find out more about reducing the impact of sequencing risk to your investments, it is highly recommended that you seek financial advice from a qualified advisor, and also that you refer to the applicable Product Disclosure Statement (PDS).

Want to know more about how Bentleys can help you?

Make a time for a chat with us today. We’re here to help you get where you want to be.

Disclaimer: This information is general in nature and should not be relied on as advice. It does not take into account the objectives, financial situation or needs of any particular person. You need to consider your financial situation and needs and seek professional advice before making any decisions based on this information.

General advice warning

The information on this website and in the articles provided are general information only and do not take into account your personal objectives, financial situation, or needs. It should not be relied on as legal or taxation advice, and it does not take the place of this type of advice. You should also read the relevant Product Disclosure Statement and Financial Services Guide before making any financial decisions.

You should consider the appropriateness of the information in light of your own objectives, financial situation, or needs before acting on it by reading a copy of the Product Disclosure Statement (PDS) and, where necessary, seek professional financial advice tailored to your personal circumstances.

Send enquiry

We’d love to hear from you. Complete the form and someone from our team will contact you soon.