Could Self-Funding Instalments Maximise Your Investment Returns?

Are you an investor in leading Australian Blue-Chip Shares and Indices? Are you keen to explore ways to maximise your investing exposure and returns?

Self-Funding Instalments are one of the limited ways that may offer you the benefits that you are seeking.

Self-Funding Instalments are a structured investment product. They offer investors and superannuation funds the potential to gain geared exposure while investing in leading Australian Blue Chips companies and indices, without the risk of a margin call.

They provide investors with a way to obtain exposure to the performance of Australia’s leading companies and indices, with the benefit of additional dividends and additional franking credits. For superannuation fund investors, this approach is one of the limited ways you can invest with leverage. (ie., borrowing).

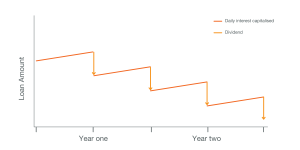

How do Self-Funding Instalments work?

For a smaller initial outlay, investors can benefit from additional franking credits and capital appreciation as if they owned the shares outright, while dividends and distributions are used to reduce the attached borrowing. At maturity, investors have the option to pay the Final Instalment and receive the Underlying Shares outright, roll over to another offering of Self Funding Instalments, or exit the investment and receive the residual value remaining.

The below illustrates how dividends are used to reduce the outstanding borrowings over time.

Source: http://www.asx.com.au

What are the benefits?

Self-Funding Instalments offer some key benefits, including

- Diversification: Because a Self-Funding Instalment requires less capital outlay, greater exposure to the underlying asset is achieved. Cash can be extracted from existing security through a Self-Funding Instalment to invest in other assets

- Dividends: During the term of the investment, a Self-Funding Instalment holder is entitled to receive all of the applicable dividends and franking credits. These dividends are used to reduce the borrowing amount of the Self-Funding Instalment. As investors only pay a smaller initial outlay for the underlying investment, the dividends of a Self-Funding Instalment can be significantly greater than that of the underlying investment

- Franking Credits: Investors may also benefit from additional franking credits, which may be especially beneficial to superannuation funds. Franking credits can be used to offset tax (and if they are not used they are refunded to the investor).

- Leverage/ Gearing: investors can leverage their existing or future shareholdings in Australian companies and indices.

- Potential tax benefits: depending on the investor status, interest expenses and borrowing fees related to the purchase of a self-funded instalment may be a tax-deductible expense

- Limited recourse: by investing in Self-Funding Instalments rather than the underlying investment, investors limit their exposure to the cost of the Self-Funding Instalment as the borrowing is non-recourse, meaning the investor never has to pay it back. This is achieved via a built in put option feature.

- Cash extraction: existing shareholders (excluding superannuation funds) can free up their capital for other investments while maintaining exposure to their shares without crystallising a capital gains tax (CGT) liability.

What are the risks?

Like any investment that offers potential for profit, there is also the potential for loss. The relevant Self-Funding Instalment product disclosure statement will detail all risks associated with investing in these types of products. The risks may include, but are not limited to, the following:

- Increased exposure: an investor will have increased exposure to a given investment. This may mean an increase in the potential of investment returns, but it may also magnify investment loss (subject to the cap provided by the put option).

- Financial performance of investment: the amount of any dividends/distributions paid by the underlying investment and applied towards the reduction of the loan is dependent on the investments’ financial performance and could decline or deteriorate. This means the attached borrowing may not be reduced to the extent anticipated.

- Increasing interest rates: as we are in a low-interest-rate environment, an increase in interest rates will result in an increase in the cost of funding the Self-Funding Instalments. This may reduce potential returns

- Change in legislation: changes to legislation and/or corporate actions may cause the completion date of a Self-Funding Instalment to be brought forward.

Key strategies for getting the most out of Self-Funding Instalments:

- Borrowing to create additional growth: investing for the medium to long-term and using borrowed funds to increase the size of the investment (and, therefore potentially the return) are two key wealth creation strategies. When sharemarkets rise, gearing using Self Funding Instalments will generally increase wealth. However, on the flip side, this approach may also magnify losses (in down markets).

- Extracting cash from your shares and using this for diversification: diversification is a key principle to managing risk in a successful portfolio. Self-Funding Instalments can help diversify your share portfolio without triggering a Capital Gains Tax (CGT) liability. This method works by freeing up capital to invest in other shares, while still maintaining exposure to the shares you originally owned (i.e., diversification). Please note that extracting cash from shares is not available for SMSFs

- Enhancing your income and potential tax outcomes: Self-Funding Instalments can potentially accelerate your investment returns by increasing your exposure for the same upfront cost. With more shares, you also have the potential to earn more dividends and benefit from additional franking credits. These additional franking credits can be used to offset income tax. Franking credits can also be very beneficial for superannuation funds.

Before considering investing in a Self-Funding Instalment, it is highly recommended that you seek financial advice from a qualified advisor, and also that you refer to the applicable Product Disclosure Statement (PDS).

Want to know more about how Bentleys can help you?

Make a time for a chat with us today. We’re here to help you get where you want to be.

Disclaimer: This information is general in nature and should not be relied on as advice. It does not take into account the objectives, financial situation or needs of any particular person. You need to consider your financial situation and needs and seek professional advice before making any decisions based on this information.

General advice warning

The information on this website and in the articles provided are general information only and do not take into account your personal objectives, financial situation, or needs. It should not be relied on as legal or taxation advice, and it does not take the place of this type of advice. You should also read the relevant Product Disclosure Statement and Financial Services Guide before making any financial decisions.

You should consider the appropriateness of the information in light of your own objectives, financial situation, or needs before acting on it by reading a copy of the Product Disclosure Statement (PDS) and, where necessary, seek professional financial advice tailored to your personal circumstances.

Reference: ASX, Self Funding Instalments, Equity Structures Products and Warrants, accessed 26 July 2021,<https://www.asx.com.au/documents/products/RBS_SFI_Brochure.pdf>

Send enquiry

We’d love to hear from you. Complete the form and someone from our team will contact you soon.